The many money challenges of women

How can women overcome money challenges and achieve financial independence?

InLife’s (Insular Life) Financial Independence Talk Series entitled “Wealth Journey: Her Way to Financial Independence” dived into the money challenges of women and presented solutions to help them achieve financial security.

Rose Fres Fausto, a behavioral economist, Gallup-Certified Strengths Coach and member of InLife Sheroes She Inspires Circle, steered the discussion by pointing out the value of FQ or financial quotient. “FQ is your ability to make sound decisions and actions with regard to your personal finances. It’s not just about finance concepts. It has to do with your behavior. FQ is the IQ and EQ of handling money,” she said.

Fausto enumerated several money challenges and countered these with solutions to help women achieve financial independence.

The book author explained that women are paid less than men for similar jobs. She noted that according to the Philippine Institute of Development Studies’ data as of 2022, the gender pay gap is around 82 centavos for women to a peso for men in digital jobs, and 92 centavos for women to a peso for men in the agricultural sector.

“Women must be very, very good with their jobs. Use your female attributes as your asset to have a better contribution to the company. If you can document all your achievements and contributions, do so. And when it's time to talk to the boss to negotiate your salary, you have great evidence,” Fausto said.

Women contend with work interruptions during pregnancy, childbirth and child rearing; abusive relationships; and taking care of the children singlehandedly in case the marriage ends.

“In a country lacking clear and easily enforceable child support policies, mothers often just must fend for their own children with little or no assistance from the estranged fathers. Sometimes it is even their choice. We often hear women say ‘I just don't want to have to do anything with the father of my children. So, I'm just gonna do it on my own,’” Fausto said.

Women endure unpaid work at home like childcare, caregiving, and household chores. Women also face resentment in case they earn more than their husbands. Fausto said these can be resolved with open discussions about money matters.

“We should have healthy and regular conversations about money with our husbands. Prepare your common balance sheet which is just a simple listing of what you own and what you owe or your liabilities or debts. Discuss equitable sharing of responsibilities, not just financial responsibilities, but also household chores and parenting,” she advised.

Build on the good traits

The natural nurturing trait of women is good for society in general, but this could pose problems when left unchecked.

“On top of taking care of their own children, women are somehow expected more than their male counterparts to take care of aging parents and other relatives who need care. And this may lead to work interruptions and additional financial burden,” she said.

Fausto said this leads to the problem of the sandwich generation or those who take care of their own family and aging parents at the same time.

“You should unsandwich yourself. Discuss the financial dependence that you’re in with your dependents and have clear terms and conditions. Up to where is their financial dependence on you? Set an expiry date on their financial dependence, otherwise you will end up having a toxic relationship,” she cautioned.

Fausto further said while women are good with budgeting, they lack confidence in investing. “Most women shy away from investing. But women have a lot of innate qualities that are important to be good investors: patience, caution and fondness for details. We need to invest. We can’t just put all our money in savings account.”

Aspire for financial happiness

On the average, women live longer than men. Fausto said this means that women must build a larger retirement nest compared to men.

Amidst these money challenges, how can women find their way to financial independence?

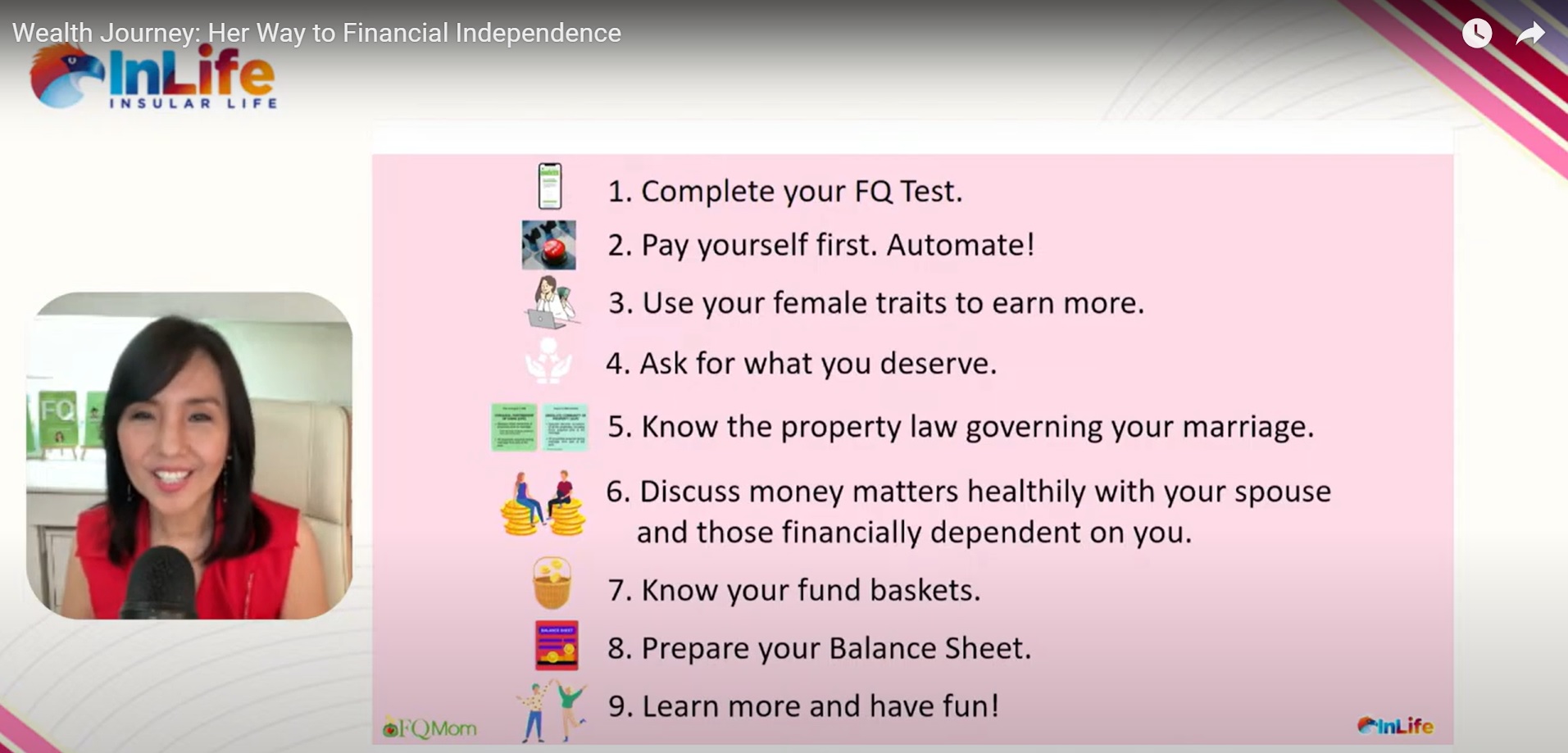

Fausto suggested completing the FQ test, paying oneself first and saving at least 20% of income automatically.

The FQ Mom advised having a short-term fund basket which pertains to a monthly budget, savings accounts and e-wallets; and building an emergency fund equivalent to 6 to 12 months of expenses which may be placed in time deposits, money market funds or higher yielding digital savings accounts. She continued that a medium-term fund basket may include a combination of fixed income and equity funds to finance five-year goals like purchasing a car or house or planning a wedding. She added that a long term fund basket may include investments in index funds and annuities to provide retirement income.

To estimate how much money may be needed for retirement, Fausto suggested multiplying the annual expenses by the estimate number of years before one goes to heaven. She also explained the three-legged stool to illustrate retirement money from three sources: the Social Security System or Government Service Insurance System benefits; retirement benefits from the employer company; and personal savings and investments.

Retire without worries with InLife. Take the first step to financial freedom, visit https://www.insularlife.com.ph/online-financial-calculator.